Jeremy Schwartz was the turnaround CEO of Pandora, the world’s largest jewellery company with 2,500 stores and e-commerce sites in 90 countries. Prior to that, Jeremy was Chairman and CEO of The Body Shop from 2013 to 2017. He also previously spent time at Sainsbury’s and, as Brand Director, he was the architect of the grocer’s turnaround in 2005 which saw a decade of growth after years in decline. He is the former Managing Director of L’Oréal UK and, as Innovation Director for Coca-Cola Europe, he invented Coke Zero. Jeremy is currently the Chairman of Kantar’s Sustainability Transformation Practice.

While watching my daughter at her gymnastics class last week, I overheard another parent talking about a kids’ birthday party they went to recently. It wasn’t the usual soft play centre but a more pleasantly scented… Lush store.

Now I must admit that, as both a retail analyst and parent, I had no idea that Lush hosted parties on its shopfloor. But it makes perfect sense – Lush isn’t just a shop but an experience. A wonderfully fragrant, sensory stimulating, bath bomb-making experience.

And that’s the kind of mentality that bricks & mortar retailers need today. You have to give shoppers something that a screen cannot. You need to embrace perpetual innovation. You need to continue to surprise and delight. And above all, as Theo Paphitis told me in an interview earlier this month, you need to have a reason to exist.

The Body Shop once had a reason to exist. Under founder Dame Anita Roddick, it pioneered ethical beauty in the 1970’s. Its focus on natural, fairtrade and cruelty-free products set the retailer apart from rivals, not to mention its strong stance on social and environmental justice issues. The Body Shop was genuinely ahead of its time.

Fast forward to 2024 and its overall proposition is still wildly relevant. The health and beauty category continues to thrive even in this tough climate and sustainable shopping has gone mainstream. And therein lies the problem. The Body Shop is no longer the only place on the high street that shoppers can turn to for ethical products. It’s not the cheapest. It’s not most convenient. And you could make the argument that it’s not the most inspiring. So what exactly is its USP?

The Body Shop may have once been a trailblazer, but they’ve settled into the status quo. Being an early mover doesn’t mean you stop moving. Standing still is the most dangerous thing you can do in retail. You have to continuously evolve in order to stay relevant to customers. If you don’t, someone else certainly will.

So how do you stay relevant in the ever-changing world of retail? Your customer should always be your North Star. Start with the customer and then work backwards. How can you elevate the customer experience? What needs aren’t currently being met? How can you ‘go beyond’?

In the beauty space, you only need to look to a brand like Rituals to see what’s possible. Their philosophy of slowing down and transforming routines into special moments is evident the minute you walk through the door. Customers receive a cup of tea or a hand massage. The store environment is calming and every product has a story. It’s unique, relevant and the perfect antidote to our fast-paced lives.

A key factor of Ritual’s success is its unique brand proposition. It views itself as a wellness and lifestyle brand, rather than a beauty brand, and therefore doesn’t see itself having any direct competitors. It also embraces technology to deliver a truly personalised experience and is continuously evolving its offer. This is how you win in retail today.

Look at some of the more notorious retail disruptors like Amazon. I’ve often attributed Amazon’s success to a relentless dissatisfaction with the status quo. Other high street retailers are now adopting a similar approach. Marks & Spencer CEO Stuart Machin refers to the business as being “positively dissatisfied” and now requires its head office staff to spend to spend a week on the shop floor. Morrisons is even inviting shoppers to join management meetings. Listening to your customers has never been more important. In today’s retail climate, no one can afford inaction.

After years of volatility and disruption, might 2024 bring some much-needed stability?

I’m optimistic that we are safely out of ‘permacrisis’ mode, but that doesn’t mean that 2024 will be uneventful. Technology will continue to disrupt the status quo, improving operational efficiencies and taking the customer experience to new heights. Here are 3 areas to watch:

AI: From Intrigue to Implementation

The buzz and excitement of generative AI bursting into the mainstream dominated the headlines in 2023, with ChatGPT alone reaching 100 million users within just a couple of months. But things will really begin to heat up in 2024: this will be the year of deployment. AI is no longer hype; it’s reality. We are on the cusp of another ‘smartphone moment’ where AI will disrupt every aspect of the value chain – from product development right through to consumption.

From a customer experience perspective, the holy grail of hyper-personalisation is finally within reach. AI-powered shopping assistants are not the future, they are here now. Rich, real-time, relevant experiences are rapidly becoming the norm. I’m personally excited to see how AI develops in our kitchens, helping consumers not only with meal inspiration but also reducing food waste, and also how AI-enabled virtual try-ons might help tackle the perennial problem of returns.

Tech-Enabled Human Touch

As retailers recognised the value in repurposed, tech-infused stores, the collective view on bricks and mortar shifted from ‘liability in a digital era’ to ‘top asset’. The industry’s primary goal of the past decade has been digitising our physical spaces. As we look ahead to the next decade, the focus will shift to making our digital spaces more physical, more immersive, more lifelike. We’re already seeing this with the rise of virtual try-ons, liveshopping, social commerce and virtual shopping consultations, to name a few. Mixed reality is coming. In the future, we really won’t know where the physical world ends and the digital one begins.

As e-commerce transitions from its current static, transactional state to one of multiple dimensions, physical retailers will need to ensure they are leveraging their staff to provide a unique, elevated experience. Retailers must look to technology here to help democratise concierge-level service, allowing staff to serve the customer in both an efficient and highly personalised way – that’s everything from clienteling to allowing customers to pay on the spot or swiftly collecting or returning an online order. Tech-enabled human touch will differentiate the winners from the losers in 2024.

ESG: Firmly Back on the Agenda

In recent years, progress on the ESG agenda may have been quietly stunted as both retailers and consumers prioritised cost efficiencies. However, it’s safe to say that this is one trend that is never going away, and I believe sustainability will be a top priority for retailers in 2024 and beyond.

Transparency will be a key theme this year. Consumers look to retailers to guide them in their decision-making and, with heightened awareness around both greenwashing and bluewashing, there is simply no hiding behind false claims or labels. Retailers will be judged on their authenticity. They should be striving for honesty over perfection. Retailers must have full visibility over their supply chain and be able to effectively communicate their practices and standards to consumers. I believe we’ll see greater demand for product durability and traceability around retailers’ broader circularity efforts. Increasingly, shoppers will want to align with brands whose values reflect their own.

Recording live from the retailer’s new Second Chance store in London, Amazon UK Country Manager John Boumphrey joins Natalie on the podcast to discuss:

How is Amazon extending the life of returned goods through its Second Chance programme?

How can the wider industry overcome the returns challenge?

Futureproofing – with more disruption on the horizon, how does Amazon ensure it stays relevant to customers?

Consumer outlook – does JB expect consumers to remain relatively resilient as we move into 2024?

From drones to generative AI: what technologies and innovations should we be watching?

Click here to display content from html5-player.libsyn.com

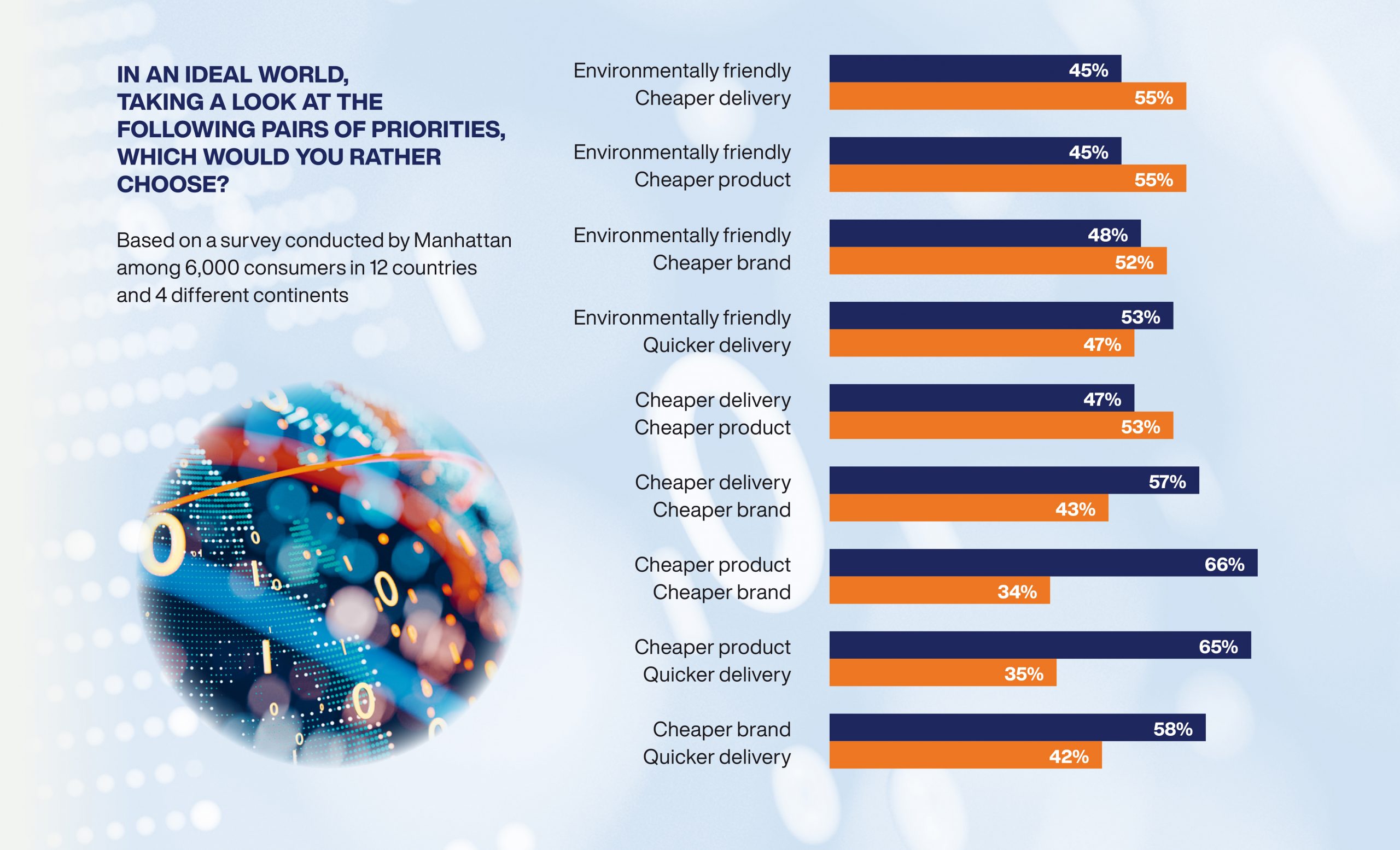

Don’t get me wrong, there still very much appears to be a desire to shop in an environmentally conscious way – but consumers are currently less willing (or able) to pay for it. Of the 6,000 global consumers surveyed by Manhattan Associates, 45% said they still consider sustainability a top or important consideration when choosing where to shop, but this is down slightly on the 50% who agreed with that statement last year.

Persistent economic concerns have curbed consumers’ appetite for sustainable shopping. In the current climate, frugality trumps sustainability. The perception, and at times reality, that green products come at a price premium has led shoppers to abandon their eco credentials to switch to low-cost alternatives.

The Manhattan survey presented consumers with pairs of priorities (ie. “cheaper” vs “environmental friendliness” in terms of brand, product and delivery) and asked them to select which they are currently choosing. Unsurprisingly, “cheaper” prevailed the majority of the time.

But challenging financial times do not impact all consumers equally. More mature demographics are likely to be most insulated, with 1 in 5 (20%) consumers aged 65 years and over reporting that there is that the cost-of-living crisis has had no impact at all on their shopping habits. Yet this is the group least likely to take sustainability into consideration when choosing where to shop: over 20% of older shoppers said that sustainability is not important or not at all a consideration for them when selecting a retailer. This contrasts sharply with the 55% of 18-24-year-olds who consider sustainability an essential or important consideration.

So what does this tell retailers? It’s never been more important to know your customer! One size most certainly does not fit all. At a strategic level, retailers need to roll out the red carpet for their most loyal customers and ensure they are living up to their brand values. At an operational level, hyper-localised product assortments and more targeted, real-time promotions will help them to cater to varying customer demands.

The whitepaper also addresses the elephant in the room – the environmental impact of e-commerce deliveries. When consumers were asked about their most important delivery consideration, only 8% cited the impact on the environment. Cost and convenience are naturally going to be top considerations, but I think the lack of transparency and awareness around the carbon impact is also a factor here. The uncomfortable truth is that retailers have spent the past decade training shoppers to expect fast and free delivery, regardless of the financial or environmental cost.

The tide, however, is beginning to turn. Some retailers have quietly started charging for delivery and returns, while others have implemented more sustainable delivery options in a bid to decarbonise the last mile. Reduced packaging for home deliveries and ‘packageless’ collections and returns are starting to gain momentum. And, with many retailers now able to provide near real-time inventory visibility, consumers can make smarter decisions about which stores to visit or which delivery options to choose, which can significantly minimise miles travelled and open up a variety of greener last-mile delivery options.

Retailers are still in the nascent stages of giving customers greater control post-purchase, but this will evolve in the future as retailers recognise the triple benefits – profits, pockets and planet. So what exactly can be done? Offering no-rush/green delivery, letting shoppers select the day of their delivery, encouraging shoppers to consolidate orders and even letting them make basket edits after the transaction. That’s right, in the future, more retailers will allow shoppers to alter online orders right up to the point a shipment leaves the warehouse, store or microfulfilment centre. With these longer ‘order modification’ grace windows, retailers can not only enhance the customer experience but also reduce split-shipments and, in theory, unnecessary returns.

Ultimately, the onus is on the retailer to initiate change. When retailers were asked to select their top 3 business priorities for 12 months, only around 1 in 5 retailers called out creating a more sustainable and environmentally aware supply chain (21%) and doing more to minimise the environmental impact of their organisation (22%).

I believe, broadly speaking, that consumers want to make better choices but the lack of awareness, lack of alternatives and perhaps a view that the onus should be on the retailer – not the consumer – to fund this shift is hindering progress. Consumers may think of themselves as altruistic – but at the sake of convenience? I don’t think so. Retailers need to become more transparent and ultimately provide consumers with compelling incentives to alter their shopping habits.

Perhaps we will only see meaningful change with regulation, but as a starting point retailers should be prioritising operational efficiencies that allow them to simultaneously progress the sustainability agenda. After all, financial and environmental sustainability often go hand in hand.

H&M is the latest fashion retailer to start charging shoppers for online returns. Jonathan De Mello, Founder & CEO at JDM Retail, joins Natalie to explore whether the days of free returns are really over. Why has bracketing (ie. buy 5 items, return 4) become normalised? Hint: retailers, you created a monster. And will charging for returns will be enough of a deterrent to reverse the buy-to-try shopping mentality?

Click here to display content from html5-player.libsyn.com

The many juxtapositions of Shein. It aims to be accessible through low pricing – but at what social and environmental cost? It launches a resale platform – but with questionable quality and an average selling price of around £5, can throwaway fashion really be resold? And now Shein has opened its first ever permanent store – but isn’t this just a ploy to grow online sales?

The Shein store launched on 13 November in Tokyo’s Harajuku fashion district. It is a significant, though unsurprising, move in the world of digitally native fast fashion. From Dallas to Dublin, Shein has experimented with a number of pop-ups around the world, where it’s had the opportunity to somewhat demystify the brand and engage with shoppers in the flesh. But, make no mistake, the real goal here is for bricks & mortar to generate a halo effect and drive e-commerce sales.

In fact, shoppers are not able to buy anything while in-store, but instead can browse clothing and scan QR codes to make an online purchase. Shein is certainly not the first online fast fashion brand to recognise the value in having a physical presence these days: here in the UK, Boohoo and Missguided have dabbled with bricks & mortar, while just last month Asos was said to be exploring the idea of opening its first UK shop in a bid to shift excess stock.

But Shein isn’t just fast fashion. It’s uber-fast – dare I say disposable – fashion. Through its “test and repeat” model, Shein is able to produce and distribute products in as little as a week. An eye-watering 10,000 new SKUs are added to the site on a daily basis and, here in the UK, it sells around 30,000 products every single day.

Cheap and cheerful may resonate with shoppers in the current climate – but certainly not all. There is a growing resistance to throwaway fashion. We’ve hit peak stuff. Shoppers are increasingly thinking twice before buying new. Resale and rental (and, to a lesser extent, repair) are becoming mainstream. We are shifting from mindless to mindful consumption. Shein, however, is the epitome of the former.

Its model of pumping out single-wear fashion to be shipped around the globe is entirely at odds with the fact that we are living in a climate emergency. And if, like me, you watched the new Channel 4 documentary on the brand’s catastrophic rise, you might have come away absolutely terrified. Our addiction to buying clothes is unsustainable.

In addition to Shein being a driving force behind the “wear-it-once” culture and contributing to environmental waste, it has also come under scrutiny for its working conditions and copyright infringement, as well as exploiting tax loopholes without which it would not be in a position to offer such cut-throat prices.

Shein is now one of the most downloaded shopping apps in the US and earlier this year, it was valued at $100 billion – essentially Zara and H&M combined. Controversies aside, Shein is a major force in the fashion world and now has its sights set on bricks & mortar. Let’s hope it cleans up its act.