In retail today, you need to have a laser-clear understanding of your brand and what it stands for.

But what if what you stand for is no longer culturally relevant? Can you shed your skin and completely reinvent yourself? Can you buy your way out of cultural insignificance?

The lingerie brand Victoria’s Secret tried to do exactly that and it hasn’t worked out so well. They’re now ready to ditch their feminist makeover and re-embrace “sex appeal”. On today’s podcast, we’re going to be exploring what went wrong at Victoria’s Secret, how they tried to fix it, and whether they can go back to their roots in a post-#MeToo world.

TLDL: Victoria Secret’s newfound conscience and subsequent brand overhaul whiffed of inauthenticity. Too much, too soon… alienating both those in favour (who perhaps questioned the integrity of such a radical makeover) and those not.

Click here to display content from play.libsyn.com

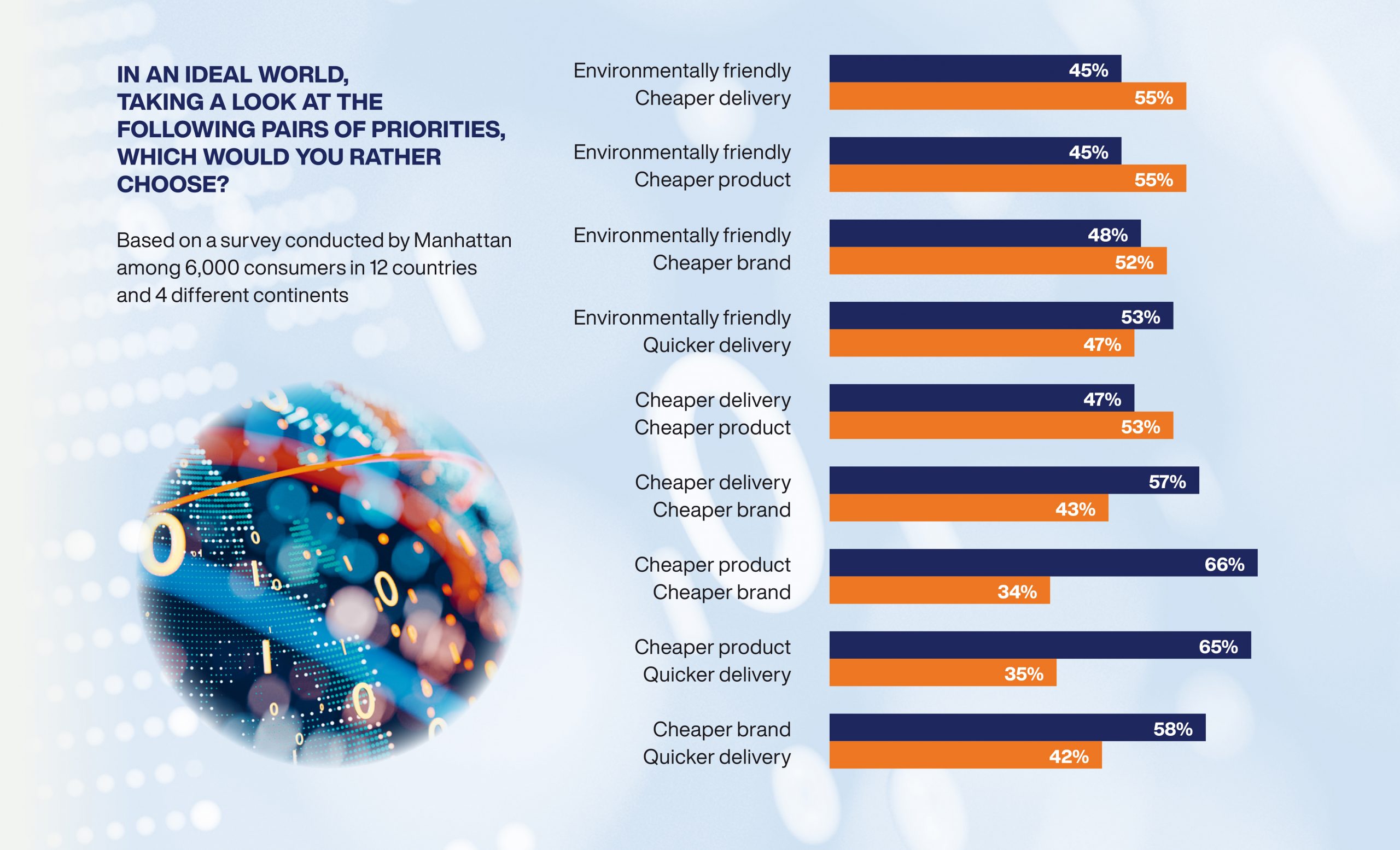

Don’t get me wrong, there still very much appears to be a desire to shop in an environmentally conscious way – but consumers are currently less willing (or able) to pay for it. Of the 6,000 global consumers surveyed by Manhattan Associates, 45% said they still consider sustainability a top or important consideration when choosing where to shop, but this is down slightly on the 50% who agreed with that statement last year.

Persistent economic concerns have curbed consumers’ appetite for sustainable shopping. In the current climate, frugality trumps sustainability. The perception, and at times reality, that green products come at a price premium has led shoppers to abandon their eco credentials to switch to low-cost alternatives.

The Manhattan survey presented consumers with pairs of priorities (ie. “cheaper” vs “environmental friendliness” in terms of brand, product and delivery) and asked them to select which they are currently choosing. Unsurprisingly, “cheaper” prevailed the majority of the time.

But challenging financial times do not impact all consumers equally. More mature demographics are likely to be most insulated, with 1 in 5 (20%) consumers aged 65 years and over reporting that there is that the cost-of-living crisis has had no impact at all on their shopping habits. Yet this is the group least likely to take sustainability into consideration when choosing where to shop: over 20% of older shoppers said that sustainability is not important or not at all a consideration for them when selecting a retailer. This contrasts sharply with the 55% of 18-24-year-olds who consider sustainability an essential or important consideration.

So what does this tell retailers? It’s never been more important to know your customer! One size most certainly does not fit all. At a strategic level, retailers need to roll out the red carpet for their most loyal customers and ensure they are living up to their brand values. At an operational level, hyper-localised product assortments and more targeted, real-time promotions will help them to cater to varying customer demands.

The whitepaper also addresses the elephant in the room – the environmental impact of e-commerce deliveries. When consumers were asked about their most important delivery consideration, only 8% cited the impact on the environment. Cost and convenience are naturally going to be top considerations, but I think the lack of transparency and awareness around the carbon impact is also a factor here. The uncomfortable truth is that retailers have spent the past decade training shoppers to expect fast and free delivery, regardless of the financial or environmental cost.

The tide, however, is beginning to turn. Some retailers have quietly started charging for delivery and returns, while others have implemented more sustainable delivery options in a bid to decarbonise the last mile. Reduced packaging for home deliveries and ‘packageless’ collections and returns are starting to gain momentum. And, with many retailers now able to provide near real-time inventory visibility, consumers can make smarter decisions about which stores to visit or which delivery options to choose, which can significantly minimise miles travelled and open up a variety of greener last-mile delivery options.

Retailers are still in the nascent stages of giving customers greater control post-purchase, but this will evolve in the future as retailers recognise the triple benefits – profits, pockets and planet. So what exactly can be done? Offering no-rush/green delivery, letting shoppers select the day of their delivery, encouraging shoppers to consolidate orders and even letting them make basket edits after the transaction. That’s right, in the future, more retailers will allow shoppers to alter online orders right up to the point a shipment leaves the warehouse, store or microfulfilment centre. With these longer ‘order modification’ grace windows, retailers can not only enhance the customer experience but also reduce split-shipments and, in theory, unnecessary returns.

Ultimately, the onus is on the retailer to initiate change. When retailers were asked to select their top 3 business priorities for 12 months, only around 1 in 5 retailers called out creating a more sustainable and environmentally aware supply chain (21%) and doing more to minimise the environmental impact of their organisation (22%).

I believe, broadly speaking, that consumers want to make better choices but the lack of awareness, lack of alternatives and perhaps a view that the onus should be on the retailer – not the consumer – to fund this shift is hindering progress. Consumers may think of themselves as altruistic – but at the sake of convenience? I don’t think so. Retailers need to become more transparent and ultimately provide consumers with compelling incentives to alter their shopping habits.

Perhaps we will only see meaningful change with regulation, but as a starting point retailers should be prioritising operational efficiencies that allow them to simultaneously progress the sustainability agenda. After all, financial and environmental sustainability often go hand in hand.

George Nott, Technology Editor at The Grocer, joins Natalie to discuss the evolution of quick commerce. They examine the latest Uber Eats / Getir collaboration, how traditional supermarkets are responding to the quick commerce trend and whether the world is ready for AI-powered conversational shopping experiences.

Fun Fact: Did you know ‘getir’ means ‘bring’ in Turkish?

Click here to display content from html5-player.libsyn.com

Live from Paris Retail Week, Natalie speaks to FreedomPay and Worldpay about unified commerce and how payments are evolving to meet customer needs. Panellists include:

H&M is the latest fashion retailer to start charging shoppers for online returns. Jonathan De Mello, Founder & CEO at JDM Retail, joins Natalie to explore whether the days of free returns are really over. Why has bracketing (ie. buy 5 items, return 4) become normalised? Hint: retailers, you created a monster. And will charging for returns will be enough of a deterrent to reverse the buy-to-try shopping mentality?

Click here to display content from html5-player.libsyn.com

“We hate Amazon. They’ll bully us and do horrible things to us. They’ll use us, we don’t want anything to do with them.” -Iceland Managing Director, 2018

Fast forward five years…

This morning Amazon UK announced that frozen food specialist Iceland will begin selling groceries on its platform. In this episode, Natalie explores the rationale behind Iceland’s shift in strategy and why Amazon is expanding its relationship with third party supermarkets like Morrisons, Co-op and now Iceland.

Amazon may need the grocery industry but does the grocery industry need Amazon? Let’s explore.

Click here to display content from html5-player.libsyn.com

Richard Hammond, CEO of Uncrowd and fellow retail author, joins Natalie to explore the differences in US and UK grocery retailing. Why have British retailers failed to crack the American market? When is it ok to have friction? Automation – how can retailers balance customer satisfaction and operational efficiencies? And what is the risk of deprioritizing CX investment in the current climate?

Listen to the end to hear Richard’s own experience of being stuck in self-checkout jail.

Click here to display content from html5-player.libsyn.com

It’s Amazon Prime Day and the bargains are flying – but will shoppers bite? What’s new this year and how has the competition responded? In this episode, Natalie also shares her views on Amazon’s latest personalisation efforts. Amazon may be the Everything Store, but it’s not exactly the Inspirational Store. How might personalised deals feeds, liveshopping and Prime Day experiences help Amazon to shift its utilitarian image?

Click here to display content from html5-player.libsyn.com

RetailNext, the leading analytics solution for bricks-and-mortar retailers, today announced that it will partner with the Retail Think Tank to produce its quarterly Retail Health Index, alongside existing co-chair and global consultant, KPMG.

First established in 2006 by KPMG and market research leader, Ipsos, the Retail Health Index is the industry’s only comprehensive, sector-level benchmark of retail performance. With almost three decades of data, encompassing pivotal moments that defined and redefined retail – from the 2008 Financial Crash and ensuing ‘Credit Crunch’ to Brexit, Covid-19, the post-pandemic recovery and, most recently, the cost-of-living crisis – the Retail Health Index assesses the sector’s key performance indicators, including demand, margin and cost.

Each quarter, it is independently scored by Retail Think Tank members – an elite advisory board comprising industry experts, thought leaders and analysts, including Nick Bubb, former GlobalData Director Maureen Hinton, and NielsenIQ’s Mike Watkins – to benchmark retail health for the past three months, and predict how performance will evolve in the next quarter. This year author and Retail Technology Magazine publisher, Miya Knights, and retail consultant and author, Natalie Berg, will join the panel as new members, bringing fresh insight and perspective to the wealth of expertise and industry know-how of the Retail Think Tank advisory board.

Following RetailNext’s acquisition of Ipsos’ people-counting and footfall solution, Retail Performance, in November 2022, which had formerly co-produced the Retail Health Index, RetailNext will now produce the quarterly index in collaboration with co-chair, KPMG.

Paul Martin, UK Head of Retail at KPMG, commented: “From its very inception back in 2006, the Retail Health Index has been a formative resource for retail businesses and leaders, aiming to quantify the knowledge of the Retail Think Tank members in a systematic way, whilst also providing an assessment of the overall retail health, for which there was traditionally no ‘official’ data.”

“Having been the voice reporting on retail health for almost three decades, we’re excited to welcome RetailNext as our co-chair for the Retail Health Index, and through the partnership we look forward to continuing to help retailers set a course for success as they navigate the multifaceted pressures, challenges and opportunities the market continues to present,” he added.

Gary Whittemore, Head of Sales, EMEA & APAC at RetailNext, commented: “With the fast-moving and multi-dimensional challenges facing retailers, impacting every area and function of their businesses, the Retail Health Index is not just a valuable indication of sector health. Crucially, it also dissects and contextualises the key factors impacting performance, drawing on the extensive knowledge and expertise of the Retail Think Tank membership. This results in a quarterly playbook for retailers, which outlines actionable insights and strategies to create competitive advantage in the context of the market, to drive retail businesses forward and readdress the balance of health back in the retailer’s favour.”

As well as being available online, a digest of the results of the Retail Health Index, including wide-ranging insight, contextual analysis and exclusive data-sets on key performance metrics, is available in a quarterly report, which is free for retailers to download.

Are the UK supermarkets profiteering? Food price inflation remains stubbornly high at 18.4% – its highest level since the 1970s – and now lawmakers want to understand if the supermarkets are lining their pockets at the expense of the shopper. In this episode, Natalie shares her views on why the grocers aren’t guilty of greedflation: they have no choice but to remain price competitive, while simultaneously doing everything in their power to protect their inherently low profit margins. Harvir Dhillon, Economist at the British Retail Consortium, joins the show to explore some of the cost pressures that retailers are facing, whether inflation has now peaked, and why a supermarket price cap is a bad idea.

Click here to display content from html5-player.libsyn.com